Languages

Thursday, July 30, 2026

News and Views from the Global South

The Tale of Two Countries: Elite Stake and Development

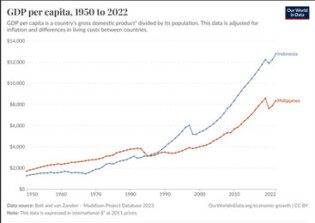

Philippines was the most advanced Southeast Asian country with the highest per capita GDP until about the early 1960s. Its per capita GDP in purchasing power parity terms were about the same as South Korea’s and above that of Thailand in the early 1970s.The Nobel Laureate economist, Gunnar Myrdal, did not have much hope for “disease infested” Indonesia when in 1968 he published his famous Asian Drama: An Enquiry Into the Poverty of Nations. But Indonesia surged ahead since the late 1960s with growth acceleration exceeding that of Philippines; thus, eventually overtaking Philippines in GDP per capita in the mid-1980s. What factors separated Indonesia from Philippines?

Social Business – It’s Time

June 27-28 is the 16th Social Business Day, observed in Savar (Dhaka) Bangladesh. In June 2024 at the Western Sydney University’s graduation ceremony where I was conferred Emeritus Professor status, I urged the new business graduates to:- • purge the world of the… obnoxious Friedmanite idea that is destroying our planet and tearing our communities apart;

• look instead to the “Social Business Model” of Bangladesh’s Nobel Laureate Muhammad Yunus; and

• work on the right side of history; stand up for justice and liberation; spread the “moral violence” for peace; and put people and the planet before profit.

World Bank Enables Corruption in Bangladesh

The World Bank considers corruption a major obstacle to eradicating global poverty. The Bank officially has a zero-tolerance policy against fraud and corruption in its projects. Concerned with widespread corruption in Bangladesh, the Bank and the Government agreed on the Governance-oriented Country Assistance Strategy (GCAS) in 2006 and the Bank’s subsequent Country Partnership Strategy (CPS) ostensibly has been more selective on governance and anti-corruption (GAC) issues. Ironically, however, the Bank’s funding enables corruption. The Bank’s recent decision to advance a US$350 million loan allegedly for enhancing energy security is a glaring example.

The Tale of Three Countries: Policy Independence Matters for Development

The Republic of Korea (Korea), Vietnam and Bangladesh are on three different rungs of the development ladder. While Korea is a member of the rich nations’ club, i.e., the Organisation for Economic Cooperation and Development (OECD), Bangladesh is still a least developed country (LDC); and Vietnam is in the middle.

Corruption in Bangladesh: Will Development Partners Remain Complicit?

Bangladesh remains one of the most corrupt countries in the world. Its corruption perception index (CPI) score, 24, is 18 points below the global average score of 42, and 21 points lower than the Asia-Pacific region’s average of 45. One of the main sources of corruption is over-priced aid-funded projects as they lack competitive bidding. Projects funded through Government-to-Government deals drive up costs by more than 400% compared to more transparent alternatives, and around 35% of project costs are lost to corruption and inefficiency.

“War-Shock Inflation” and Inflation Phobia: Lessons of History for Central Bankers

The global economy, is at the precipice of “stagflation” – growth slowdown and higher inflation – due to the energy price shock following the illegal US-Israel war on Iran. The International Monetary Fund (IMF) has recently termed this as a “textbook negative supply shock”. For the first time since the 1970s, the prospect of stagflation seems real.

The Political Economy of Bangladesh’s LDC Graduation

Bangladesh is scheduled to graduate from the least developed country (LDC) status in November this year after more than half a century. Bangladesh joined the UN club of LDCs in 1975 and consistently met all three graduation criteria – per capita Gross National Income (GNI), human asset and economic vulnerability – since 2018.

A Year of High Expectations and Frustrations

As many of you know, out of the blue, I have been called in to assist the Interim Government led by Nobel Laureate Professor Muhammad Yunus in stabilising the economy left in ruins by the fallen autocratic-kleptocratic regime that looted the banks, stole public money and robbed small investors in the capital market to siphon off billions of dollars out of the country. I had never served in a government; neither had I ever expected this opportunity. However, my UN experience and political economy understanding have been handy.

Bangladesh Economy: Turning Demographic Challenges into Opportunities

Speaking at the recent annual conference of the Bangladesh Administrative Service Association, Chief Adviser Dr Muhammad Yunus has emphasised the need to create opportunities for young people, asserting that Bangladesh’s large population is not a burden but a valuable resource.

The Year 2024: Hopes & Despairs

Thank God, we have survived another year of genocide, war, destruction and climate crisis. The passing year of 2024 has been a mixture of hope and despair. It began with some hope as the International Court of Justice (ICJ) ruled in favour of South Africa’s case against Israel for committing genocide and ordered Israel to take all measures within its power to prevent the commission of all acts within the scope of Article II of the Genocide Convention, and to take immediate and effective measures to enable the provision of urgently needed basic services and humanitarian assistance to address the adverse conditions of life faced by Palestinians in the Gaza Strip.

Bangladesh in Crisis: Which way out?

This piece is not about the crisis or the chaos that the country is now facing after successfully toppling the autocratic regime of Sheikh Hasina. Rather, it is about the crisis of confidence and social capital or trust — interlinked, nonetheless.

Climate Justice Needs Recognition of Common, but Differentiated Responsibilities

Climate justice recognizes differential impacts of climate crisis between rich and poor, women and men, and older and younger generations. The UN Secretary-General António Guterres emphasized, “as is always the case, the poor and vulnerable are the first to suffer and the worst hit.” However, all people should have the agency to live life with dignity. Thus, climate justice looks at the climate crisis through a human rights lens.

Odious Debts: What Can Bangladesh Learn from Ecuador?

Bangladesh’s White Paper committee will review foreign loan deals signed by the fallen kleptocratic regime. We recommend that it identifies and declares the loans or portions of loans that did not benefit the nation as unpayable, because they were siphoned off the country by corrupt politically powerful elites, or worse used to buy deadly weapons and surveillance equipment to oppress people. Such loans are “odious” – they stink and are detestable.

Recovering stolen assets: No weakening of resolve

The White Paper on the state of Bangladesh’s economy will include a review of “smuggled money”, according to the head of the committee, Debapriya Bhattacharya, entrusted to prepare the White Paper.

Recovering Bangladesh’s Stolen Wealth

Bangladesh bleeds as over US$3 billion drains from Bangladesh annually through offshore accounts. According to a recent report, close to US$150 billion was siphoned off the country during 15 years of kleptocratic Hasina regime’s mis-rule. Nearly US$50 billion went out of the country in the first six years (2009-2015) of the Hasina regime.

Dealing with Bangladesh’s Odious Debt

Bangladesh has become increasingly indebted since 2009. The country’s external debt stock increased from US$23.3 billion in 2008 to US$100.6 billion in December 2023 (see figure below). Thanks to the country’s mega-projects led so-called development with borrowed money under the now deposed authoritarian regime of Sheikh Hasina.

The Demise of Democracy and Human Rights Violations in Bangladesh: International Financial Institutions’ Culpability

The International Monetary Fund (IMF), World Bank and Asian Development Bank (ADB) are complicit in the gross human rights violations and death of democracy in Bangladesh. They continued to supply financial blood line to the regime, well-documented for its corruptions, human rights violations – such as forced disappearances and tortures in custody – and riggings of votes, including politicization of state institutions in its slide into autocracy. This is despite their professed commitment to transparency, accountability and good governance (IMF, World Bank, ADB).

A Bleak Future 50 Years after the New International Economic ‘Non-order’?

Fifty years ago on 1 May 1974, the Sixth Special Session of the General Assembly (April–May) adopted a revolutionary declaration and programme of action on the establishment of a New International Economic Order (NIEO) “based on equity, sovereign equality, interdependence, common interest and cooperation among all States, irrespective of their economic and social systems”. The hope was that a NIEO would “correct inequalities and redress existing injustices, make it possible to eliminate the widening gap between the developed and the developing countries and ensure steadily accelerating economic and social development and peace and justice for present and future generations”. Alas, what evolved is far from what was envisioned or called for.

Gaza Massacre and Western Hypocrisy

Israeli troops opened fire targeting the Palestinians, gathered around food aid trucks, killing at least 112 and injuring hundreds on 29 February. The massacre happened, about a month after the International Court of Justice (ICJ) ordered provisional measures for Israel to refrain from all acts under the Genocide convention. Ironically Israel was supposed to report to the Court, within one month, of all measures taken in line with its order. Israel has been emboldened by a beholden US.

‘Unbounded’ Impunity Emboldens Israel

Israel continues to reject calls for a ceasefire in Gaza and now readies itself for an assault on Rafah with a Ramadan deadline for the release of all hostages. It emphatically says, it will oppose any international attempt at creating a Palestinian State, regarded as an “unilateral recognition”. Its unrestrained bombings and ground assaults so far have resulted in close to 30,000 Palestinian deaths more than half of whom are women and children. they have brazenly ignored the International Court of Justice (ICJ) order to take all measures to prevent a plausible genocide. Many thousands are facing starvation and death even when the United Nations Security Council (UNSC) demanded unhindered aid flows to besieged Gaza. All these were possible due to Israel’s ‘unbounded’ impunity which emboldens it.

The West’s Frankenstein Moment

Israel continues to defy its strongest backer the US and its western allies in its quest to control the land from the “River to the Sea”, and in the process ethnic cleansing of the Palestinian population. Israel’s Prime Minister Benjamin Netanyahu is determined to push ahead with a ground offensive against Gaza’s southernmost town of Rafah despite mounting warnings from aid agencies and the international community that an assault on Rafah would be a catastrophe. He also snubbed the US on the latest hostage release and ceasefire deal brokered by Qatar and Egypt. The interim order of the International Court of Justice (ICJ) to take all effective measures to stop “plausible” genocide in Gaza seems irrelevant to Israel. Josep Borrell, the EU’s foreign policy chief admits that Netanyahu “doesn’t listen to anyone”.Next Page »

The Week with IPS

NEXT STOP - SDGs

Tracking global progress towards a sustainable world

Tracking global progress towards a sustainable world